Federal banking regulations, such as this FDIC regulation, mandate the confidentiality and non-discoverability of suspicious-activity reports (SAR) without mentioning the word “privilege.” As you can read more about in 1-6 Privileges & Protections: TN & Sixth Circuit Law § 6.05 (2024), many courts have nevertheless ruled that these regulations create an evidentiary privilege that prohibits either a bank or a banking regulator from disclosing a SAR or information about the filing or non-filing of a SAR.

So, how do these SAR regulations play out during discovery and trial? The court’s decisions in Camenisch v. Umpqua Bank, 2025 U.S. Dist. LEXIS 9755, provide an outline. In this case, the court reviewed several banking documents in camera and ruled that some, but not all, fell within the SAR privilege’s scope. And just before trial, it precluded the parties, including plaintiffs’ expert, from mentioning SAR-related information while permitting them to discuss the bank’s investigative efforts. And because these restrictions and permissions may result in the jury hearing less than the full story, the court decided to inform the jury, through a special instruction, why federal SAR regulations precluded them from hearing more. Let’s look at the details.

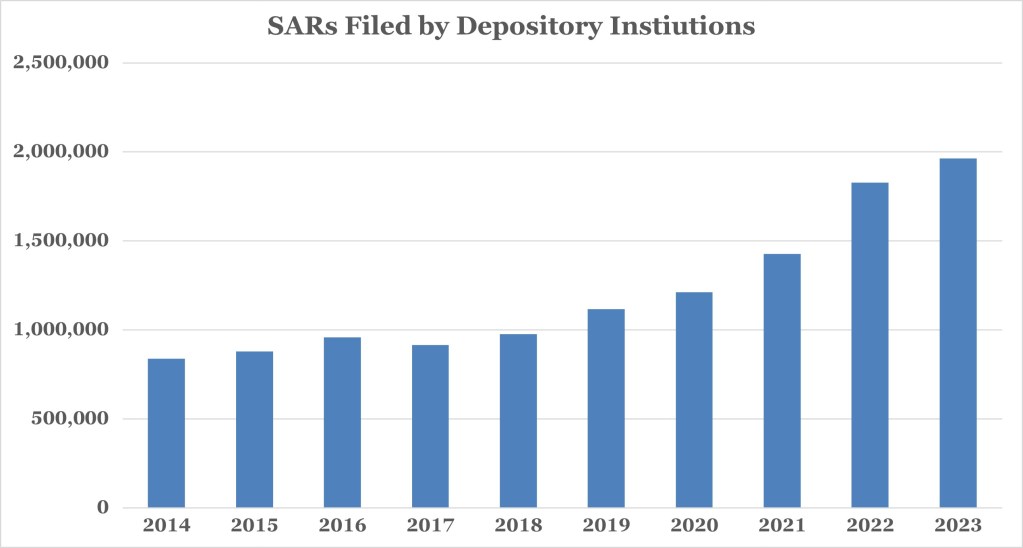

Increase in SARs

While a relatively obscure evidentiary privilege, the SAR privilege may attract courts’ increased attention in the years ahead. As reported by FinCEN, and summarized in the chart below, depository institutions more than doubled their SAR filings over the last decade, with significant increases in 2022 and 2023.

One can reasonably assume that criminal and civil litigation will erupt from activities underlying these filings and, if so, lawyers and courts will have to maneuver through the SAR privilege with more frequency than ever before. Perhaps the Camenisch case will offer some guidance.

A Class Action and Banking-Industry Expert

Several investors in a real-estate investment fund filed a class-action lawsuit against Umpqua Bank after sustaining losses. The investment fund’s founders, as it allegedly turned out, lost money and began a Ponzi scheme through which it used new investor money to pay prior investors. The scheme unraveled and, with one owner dead, another in prison, and the fund in bankruptcy, the investors turned to Umpqua Bank for relief.

The plaintiffs-investors claim that the bank had knowledge of the Ponzi scheme, due in part to many “red flags” on the investment fund’s account, but failed to do anything about it. The plaintiffs disclosed a banking-industry expert, a former state banking commissioner, to offer opinions on typical practices in the banking industry, which transactions lack business justification, and the types of customer behavior that banks should consider so-called red flags.

Umpqua denies plaintiffs’ assertions and the case is currently headed to trial as a certified class action for reasons you can read about in this court order.

Discovery of SAR Information

During discovery, plaintiffs requested information related to suspicious-activity alerts arising from the investment fund’s account and the bank withheld over 100 documents on the basis that the SAR privilege precluded production. The court, citing an OCC regulation (12 C.F.R. § 21.11(k)), stated that “[a] SAR, and any information that would reveal the existence of a SAR, are confidential, and shall not be disclosed.” But how does one apply this privilege in practice?

Citing the First Circuit’s opinion in In re JPMorgan Chase Bank, N.A., 799 F.3d 36, 2015 U.S. App. LEXIS 14721, the court, in an opinion available here, held that “the key query” in assessing the SAR privilege’s scope is whether the document “suggest[s], directly or indirectly, that a SAR was or was not filed.” Despite the bank’s contrary arguments, this standard does not protect all documents underlying a SAR and provided this example—

Some bank prepared documents may simply aggregate relevant account or transactional information, flag potentially suspicious activity that needs to be investigated further, or explain what steps need to be taken as part of that investigation. Documents like these may reflect the bank’s due diligence, but they won’t always shed light on whether or not a SAR was filed.

And using these standards, the court reviewed the bank’s 100+ documents in camera and determined that only 12 fell within the SAR privilege

Expert Opinion Restrictions and an Explanatory Instruction

Having achieved some SAR privilege success in the discovery phase, the bank became concerned that, if plaintiffs’ banking-industry expert testified that the bank performed no investigation in response to anti-money laundering alerts, it could not use the SAR-privileged information to show how it actually investigated those alerts. The bank therefore moved to exclude the expert’s opinion regarding the bank’s investigation efforts.

The court, in an opinion available here, again noted the SAR privilege’s narrow application, stating that the privilege “only extends to testimony that would reveal the filing or non-filing of an SAR.” This privilege does not, according to the court, “encompass the details of an investigation leading to the decision whether to file a SAR.”

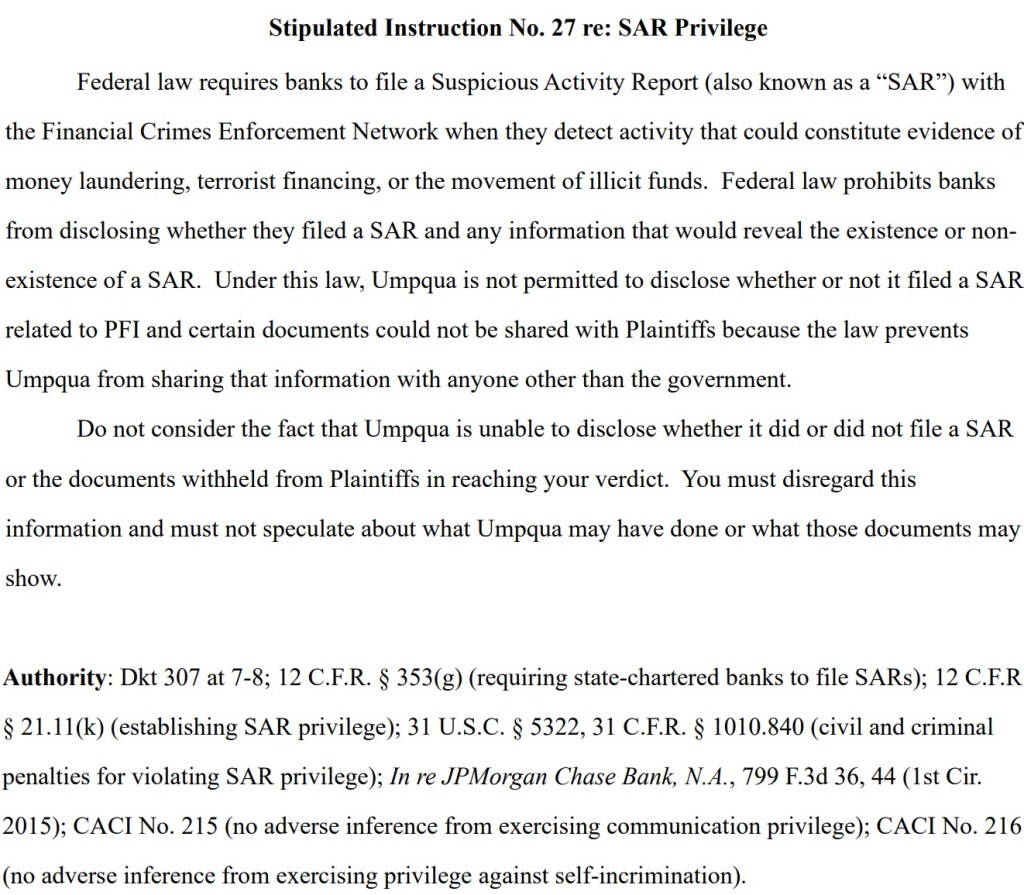

The court therefore allowed both parties to introduce testimony about the bank’s investigations but stated that it would—before any such testimony—provide the jury with an instruction that the SAR privilege prevents the bank from revealing whether it filed a SAR in connection with any investigation and that it withheld certain documents from plaintiffs due to the SAR privilege. The parties then worked together and proposed this joint jury instruction:

In the short term, we will see how this jury deals with explanations of the SAR privilege and in the long term, we may see how other lawyers and courts handle what could be an increase in SAR privilege claims.

grand! TikTok Banned in Another Country Over Data Privacy Concerns 2025 magnificent